US Spending & Tax Collections post-TCJA

According to a preliminary analysis by the Congressional Budget Office, the federal government’s deficit in fiscal year 2024 ended in September at $1.8 trillion, lower than the $1.9 billion deficit CBO predicted in June.

Revenues were slightly higher than expected and spending was slightly lower. The deficit in FY24 was about 6.4 percent of GDP after accounting for recent revisions and expected economic growth. This is larger than any deficit recorded since 1930 except the years around World War II, the 2008 financial crisis, and the pandemic. The net interest on public debt, which increased by 34 percent in FY24 to $950 billion, is a major contributor to the growing deficit. Interest on the debt has now become the second largest federal expense after Social Security which costs $1.5 trillion. This is more than defense spending of 826 billion dollars and Medicare spending $869 billion. Interest paid on the debt was 3.3 percent of the GDP in FY24, which is the highest ever recorded (after adjustments to compare). This would be the first time since 1992 that interest has been measured in this way. Interest on the debt as a share of GDP is set to enter unchartered territory in the new fiscal year, surpassing the high-water mark set in the early 1990s.Another growing part of the budget, technically scored as spending, is refundable tax credits, including the Affordable Care Act’s health insurance premium

tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. Tax credits are different from deductions and exclusions, which directly reduce the tax bill of a taxpayer, not their taxable income.

These items grew 16 percent to $199 billion in FY24.

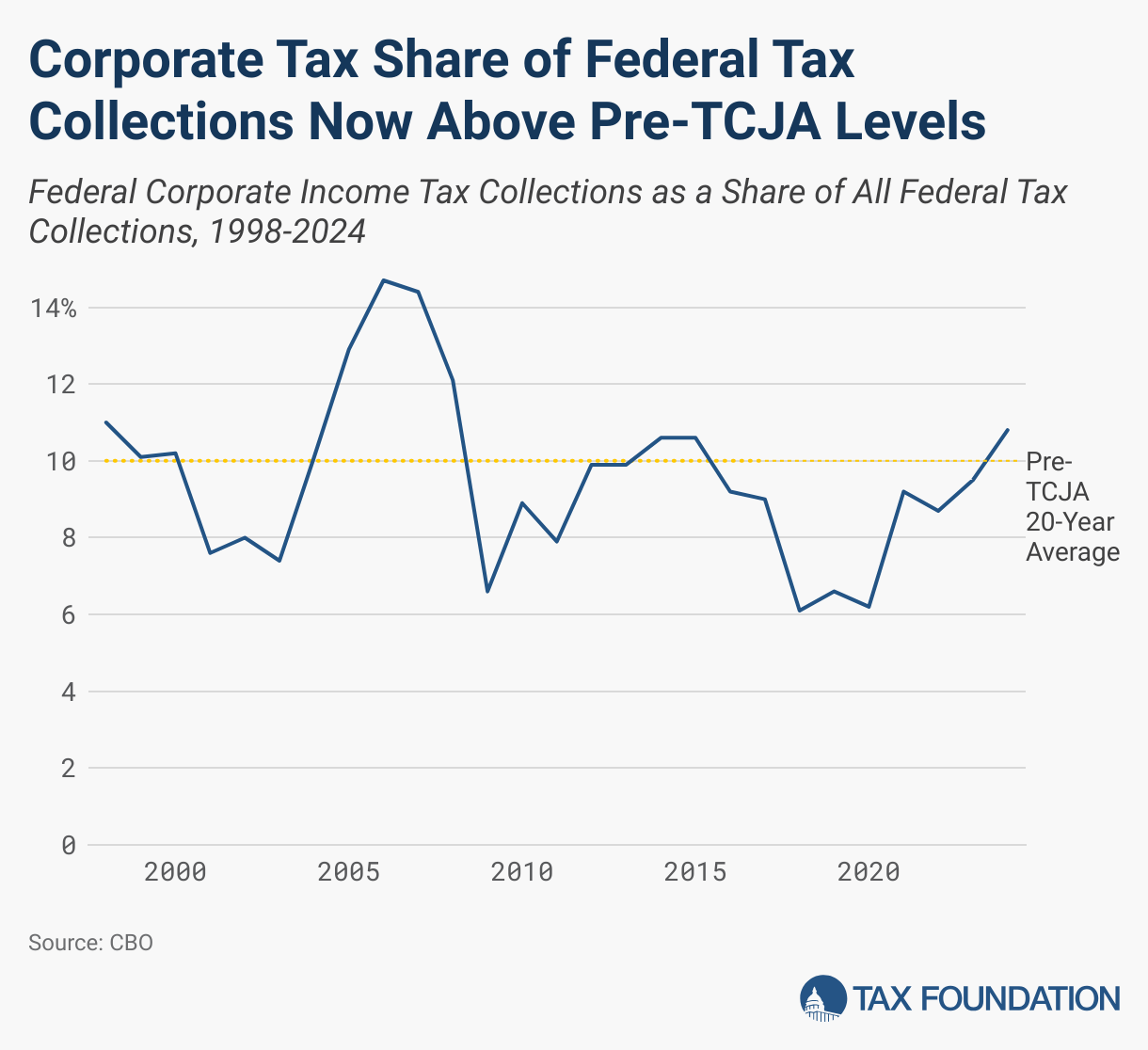

Other major spending categories grew more modestly, though there is considerable uncertainty about the impact of the administration’s policy on student loan forgiveness. These items grew by 16 percent in FY24 to $199 billion. However, there is still uncertainty regarding the impact of the policy on student loans. CBO notes that the budget totals do not include the latest student loan policy announced in April because it is in litigation, but if finalized, the rules could add more than $100 billion to this year’s deficit.Overall, CBO estimates spending grew 10 percent in FY24 to $6.8 trillion. Federal spending in FY24, at about 23.4 per cent of GDP, was higher than the 20-year average. As a percentage of GDP, federal tax collection reached 17.1 percent. This is higher than the previous 20-year average of 16 percent and similar to the average for the 20 years before the 2017 Tax Cuts and Jobs Act. Since the TCJA, federal tax collections have averaged 17 percent of GDP.The biggest source of revenue is individual income taxes which grew by 11 percent in FY24 to $2.4 trillion, while payroll taxes grew by 6 percent to reach $1.7 trillion. The fastest-growing revenue source was corporate income tax, which grew by 26 percent to $529 Billion. This is 109 Billion dollars higher than the previous year and the highest year ever. Other receipts increased 12 percent to $255 billion. Even after adjusting for this shift, the growth of corporate tax revenues is still notable. The average corporate tax collection over the last two decades was $474 billion. This is $49 billion more than the previous record of $425 billion set in 2022.

As a percentage of GDP, corporate taxes collections in FY24 reached 1.8 percent, the highest since 2015, and above the 1.7 per cent average of the 20 years before the TCJA. Averaging over the last two years, corporate tax collections have been about 1.7 percent of GDP, roughly matching the pre-TCJA average.

Other measures indicate corporate tax collections are at or above historic levels. Corporate tax collections accounted for 10.8 percent of federal tax revenues in FY24. This was the highest share since 2008 The main reason for this is that TCJA reduced the corporate rate and also significantly broadened the tax base. The tax base is the amount of income, assets, consumption or transactions that are subject to taxation. A narrow tax base can be inefficient and non-neutral. A broad tax base allows for lower tax rates and reduced administration costs.

. The Joint Committee on Taxation (JCT) estimated that these offsets would raise more than $1 trillion over a decade, offsetting more than three-quarters of the $1.3 trillion cost of reducing the corporate tax rate. The TCJA reforms also changed the timing of tax collection, pushing it into the future. The policy of 100 percent

bonus DepreciationBonus Depreciation allows firms a greater portion of their “short-lived investments” in new or improved technology or equipment or buildings to be deducted in the first year. Businesses can write off more investments, which helps to reduce a bias in tax laws and encourages them to invest more.

, that began to phase out in 2023 shifted capital investment deductions forward. In 2022, the business tax rate increased as R&D amortization was implemented and interest limitations were tightened. JCT estimated the TCJA business and international reforms will initially reduce revenue, but increase revenue net by 2023. This would result in a net revenue gain $21 billion by 2024. We found similar results in our modeling.

Another reason corporate tax collections have grown so much is that TCJA reforms boosted economic growth and profits while encouraging companies to report more profits for tax purposes. The original JCT score did not take into account economic growth. However, it did predict how companies would report profits from domestic sources to the IRS. CBO and we both estimated that TCJA would increase economic growth, the corporate profits tax base, and corporate tax revenues in 2018. However, we underestimated how much revenue would grow. CBO predicted that corporate tax collections for this year would reach 1.6 percent, but they actually reached 1.8 percent. Studies indicate TCJA did in fact strongly boost business investment and economic growth over the last few years.

As discussed in an earlier analysis, federal tax collections as a whole in recent years have surpassed our 2017 projections of both static and dynamic revenues under TCJA, even after accounting for

inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck will cover less goods, bills, and services. It is sometimes called a “hidden” tax, as it makes taxpayers less wealthy due to increased costs and “bracket-creep”, while increasing government spending power.

. The IRA introduced a corporate alternative minimum tax (AMT), a stock-buyback tax and several green energy credits. Although the net revenue effect of these measures has been difficult to determine, they likely resulted a net corporate income tax cut. Immigration may have also boosted corporate tax revenues. Some of this strength is expected, as it was a part of the TCJA design, including offsetting revenue raisers and timing shifts. Other intervening factors are also responsible for some of this strength. Nonetheless, growth in spending, particularly interest on the debt, has swamped much of these gains, producing another year with an alarmingly high deficit.Stay informed on the tax policies impacting you.Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe to our Newsletter

Share this articleTwitter

Facebook Email