Biden State of the Union Address: Tax Proposals

President Biden’s 2024 State of the Union Address presented a vision of higher taxes for American businesses and high earners combined with carveouts, credits, and more complex rules for taxpayers at all income levels. Rather than aiming for a simpler tax code that broadly encourages investment, saving, and work in the United States, the president has promised higher taxes that would decrease economic output and incomes, reduce U.S. competitiveness, and further complicate the taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

code.

The tax changes Biden proposes fall under three main categories: additional taxes on high earners, higher taxes on U.S. businesses—including increasing taxes that Biden enacted with the InflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck covers less goods, services, and bills. It is sometimes referred to as a “hidden tax,” as it leaves taxpayers less well-off due to higher costs and “bracket creep,” while increasing the government’s spending power.

Reduction Act (IRA)—and more tax credits for a variety of taxpayers and activities. The combination of policies would move the tax code further away from simplicity, transparency, and neutrality.

President Biden reintroduced his proposal to raise the effective tax rates paid by households with net worth over $100 million. The proposal requires these households to pay a 25 percent minimum tax rate on an expanded definition of income that includes unrealized capital gains. This means these households would pay tax on capital gains even if the underlying asset has not yet been sold, operating as a prepayment for future capital gains taxA capital gains tax is levied on the profit made from selling an asset and is often in addition to corporate income taxes, frequently resulting in double taxation. These taxes create a bias against saving, leading to a lower level of national income by encouraging present consumption over investment.

liability.

The billionaire minimum tax as it is commonly known would increase the complexity of the tax code by using a non-traditional and difficult-to-measure definition of income. It would require formulaic rules for valuing different types of assets, payment periods that vary by asset type, and a separate tax system to deal with illiquid assets. This tax design goes well beyond international norms, where capital gains are taxed when realized and at lower rates than the U.S. in many cases.

Aiming to address Medicare’s growing budgetary shortfalls, the president would raise the hospital insurance (HI) payroll taxA payroll tax is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security, Medicare, and unemployment insurance. Payroll taxes are social insurance taxes that comprise 24.8 percent of combined federal, state, and local government revenue, the second largest source of that combined tax revenue.

for those earning over $400,000 from 0.9 percent to 2.1 percent. The net investment income tax (NIIT), a 3.8 percent tax on passive investment income for those earning over $200,000 (single) or $250,000 (joint), would be expanded to include active business income. This change would raise top tax rates on labor and business income while not doing enough to put entitlements on a path toward solvency.

President Biden also committed to preserving the additional funding appropriated to the Internal Revenue Service (IRS) as part of the Inflation Reduction Act. Biden argues this would help raise revenue from higher earners who evade taxes and would also improve taxpayer services. Much of this new revenue may take time to appear as the IRS trains new staff and spends time identifying evasion and enforcing the tax law. However, the other components of Biden’s tax plan will push the code in a more complex direction, making the job of the IRS to enforce the law more difficult.

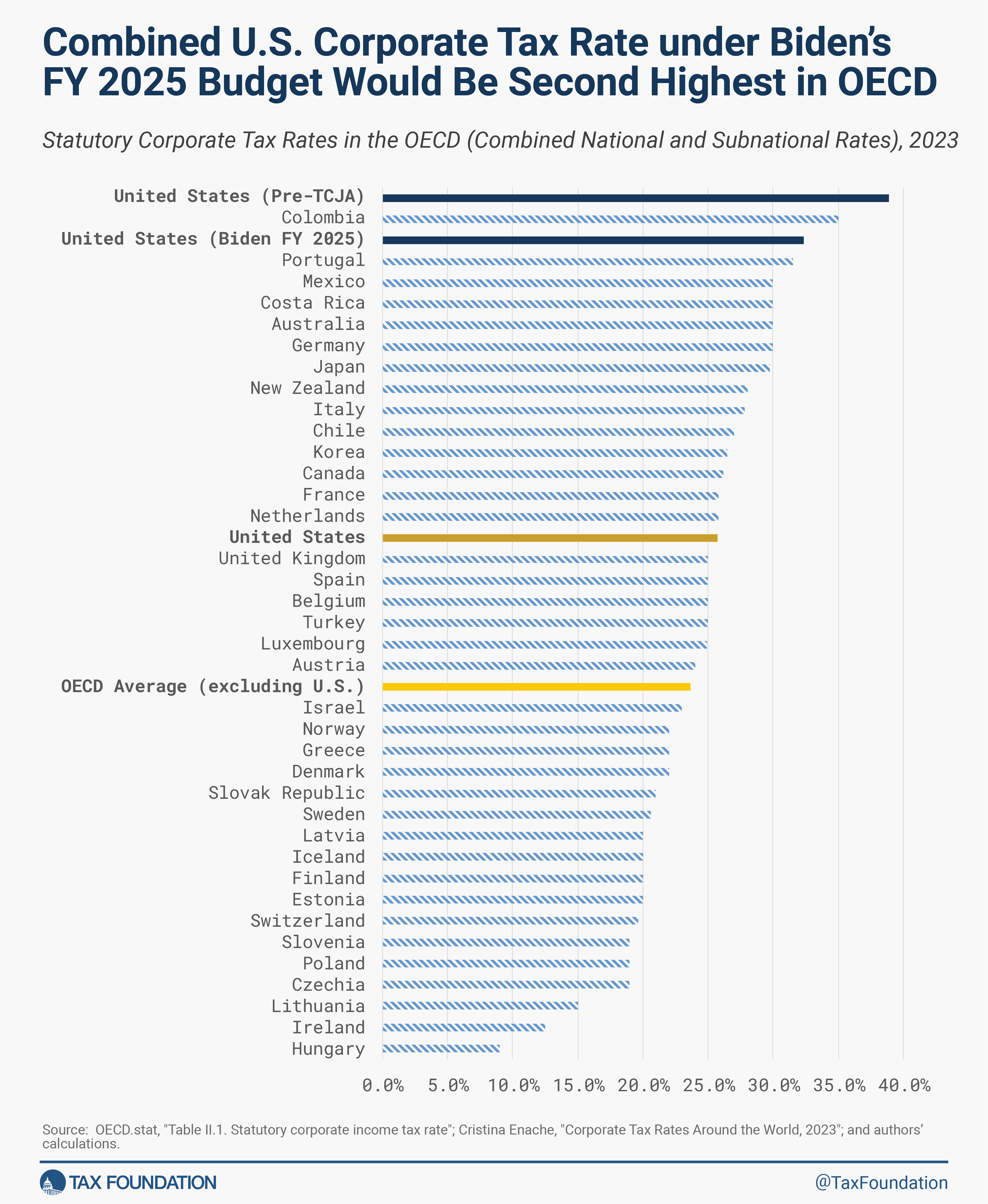

President Biden proposed to raise the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.

rate from 21 percent to 28 percent, a policy he has pushed for since the 2020 campaign. The corporate income tax is the most harmful tax for economic growth and its many problems have led countries around the world to reduce corporate tax rates considerably over the last 40 years to an average of about 23 percent as of 2023. The U.S. had the highest corporate tax rate in the OECD prior to the 2017 Tax Cuts and Jobs Act (TCJA), which lowered the U.S. corporate tax rate to be roughly average among OECD countries. Recent studies have determined that lowering the corporate tax rate significantly boosted investment in the United States, a long-term process that continues to yield economic benefits, including gains in workers’ wages.

Raising the corporate tax rate from the current 21 percent to 28 percent, combined with the average state-level corporate tax rate, would give the U.S. the second-highest combined corporate tax rate in the OECD, significantly worsening the competitive position of U.S. businesses and reducing prospects for business investment and workers.

On top of a higher statutory corporate tax rate, Biden has proposed increasing the rate of the new corporate alternative minimum tax (CAMT) on book incomeBook income is the amount of income corporations publicly report on their financial statements to shareholders. This measure is useful for assessing the financial health of a business but often does not reflect economic reality and can result in a firm appearing profitable while paying little or no income tax.

from 15 percent to 21 percent. The tax was enacted in August 2022 as part of the Inflation Reduction Act and scheduled to go into effect starting in 2023, but the IRS postponed its implementation because of the complexity of enforcing it. Taxpayers are still awaiting guidance on several significant questions related to the CAMT, and it remains questionable whether the tax is even feasible. It has certainly failed thus far as an effective minimum tax.

Biden also proposed quadrupling the IRA’s 1 percent excise taxAn excise tax is a tax imposed on a specific good or activity. Excise taxes are commonly levied on cigarettes, alcoholic beverages, soda, gasoline, insurance premiums, amusement activities, and betting, and typically make up a relatively small and volatile portion of state and local and, to a lesser extent, federal tax collections.

on stock buybacks. Stock buybacks are one of the ways businesses return value to their shareholders. Companies can return earnings to shareholders by issuing dividends (namely cash payments) or with stock buybacks (purchasing shares of their own company). As much as 95 percent of the money returned to shareholders from stock buybacks subsequently gets reinvested in other public companies. Quadrupling the tax rate would likely discourage firms from pursuing stock buybacks, potentially tilting toward more dividend issuances instead, and could discourage investment.

The final corporate tax hike Biden previewed in his State of the Union address is to expand the cap on deductions for employee compensation above $1 million (Section 162m). The cap currently applies to the CEO, CFO, and the next three highest-paid employees of a corporation, and due to the American Rescue Plan Act (ARPA) is already scheduled to expand to the next five additional highest-paid employees beginning after 2026.

Biden’s proposal would expand the cap to cover all employees, raising the cost of compensating employees and making it costlier for corporations to attract and retain top talent. It would mean both the corporate and individual top tax rates would apply to wages, resulting in top tax rates of 70 percent or more including state taxes. If the $1 million threshold is not indexed to inflation, over time the tax would hit more than just the C-suite.

Biden has called for several proposals to subsidize home purchases and boost the low-income housing tax creditA tax credit is a provision that reduces a taxpayer’s final tax bill, dollar-for-dollar. A tax credit differs from deductions and exemptions, which reduce taxable income, rather than the taxpayer’s tax bill directly.

, including a tax credit worth $5,000 per year for two years for middle-class, first-time homebuyers. The president would also offer a one-year tax credit worth up to $10,000 for middle-class households who sell a starter home to help improve starter home availability. Finally, the president proposes to provide up to $25,000 in down payment assistance for first-generation homebuyers.

Boosting demand through subsidies is likely to cause housing prices to increase further. What is needed is a greater supply of housing, which would be best accomplished at the state and local level by reforming zoning rules and at the federal level by reforming tax depreciationDepreciation is a measurement of the “useful life” of a business asset, such as machinery or a factory, to determine the multiyear period over which the cost of that asset can be deducted from taxable income. Instead of allowing businesses to deduct the cost of investments immediately (i.e., full expensing), depreciation requires deductions to be taken over time, reducing their value and discouraging investment.

rules for residential structures.

For developers, the president would expand the low-income housing tax credit (LIHTC) and create a new neighborhood homes tax credit to build or renovate affordable houses. This approach would be an inefficient way to build new homes as the existing LIHTC is expensive for the homes produced, with much of the credit value going to developers and financing agencies.

President Biden would renew the expanded child tax credit (CTC) from the 2021 American Rescue Plan Act, which would raise the CTC value from $2,000 to a maximum value of $3,600 while removing work and income requirements. This CTC expansion would have major fiscal costs totaling over $1 trillion over 10 years above the current policy CTC. If we include the underlying CTC expansion from the Tax Cuts and Jobs Act that expires at the end of 2025, the cost would approach $2 trillion over 10 years.

In addition to the CTC expansion, the president would expand the earned income tax credit (EITC) and would make permanent the expanded Affordable Care Act (ACA) premium tax credits that are scheduled to expire at the end of 2025.

Finally, the president recommitted to not raising taxes on those earning under $400,000, arguing that he would fully pay for expiring TCJA individual tax changes with “additional reforms” that would further raise taxes on high earners and businesses. These unspecified reforms would need to total at least $1.4 trillion to cover TCJA extension for those earning under $400,000.

The president’s tax policy proposals as outlined in the State of the Union address would make the tax code more complicated, unstable, and anti-growth, while also expanding the amount of spending in the tax code for a variety of policy goals not related to revenue collection.

If the president also commits to substantial new spending to be covered by further unspecified tax hikes, this could amount to a record number and size of proposed tax hikes within the president’s FY 2025 budget that will be released next week. Large tax hikes focused on businesses and the top 1 percent of earners would put the U.S. in a distinctly uncompetitive international position and threaten the health of the U.S. economy.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

Share