The Meals Tax Rates of US Cities

Food consumption is generally associated with economic progress, prosperity, and higher standards of living. Economic progress, prosperity, and higher standards of living are generally associated with food declining as a share of consumption.

Fifty years ago, food purchased for home consumption and food services (mostly in the form of prepared food and restaurant meals) accounted for 18.8 percent of personal consumption expenditures in the United States. In 2023, only 12.9% of personal consumption expenditures will be attributed to food. The composition of food consumption is also changing dramatically. In 1973, 68.5 percent (in monetary value) of food expenditures were for home consumption. By 2023, the figure had dropped to 51 percent. Prepared meals accounted last year for 49 percent of all food expenditures. In 2022, the consumer spending on food services in nominal terms reached $1 trillion for the first time ever in the history of the country. By 2023, due to

inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck will cover less goods, bills, and services. It is sometimes called a “hidden” tax, as it makes taxpayers less wealthy due to increased costs and “bracket-creep”, while increasing government spending power.

This trend towards restaurant meals and prepared food offers state and local policymakers an opportunity to generate more

tax. A tax is a mandatory payment collected by local, national, and state governments from individuals and businesses to cover costs of general government goods, services, and activities.

With relatively little effort, you can generate revenue. In most US states prepared food is subject to the general sales taxes. This is unlike food purchased for home consumption which is often exempt from tax. Many governments exempt items like groceries. Broadening the base, by including groceries, would allow rates to be lower. A sales tax should exclude business-to-business transfers that, when taxed cause tax pyramiding.

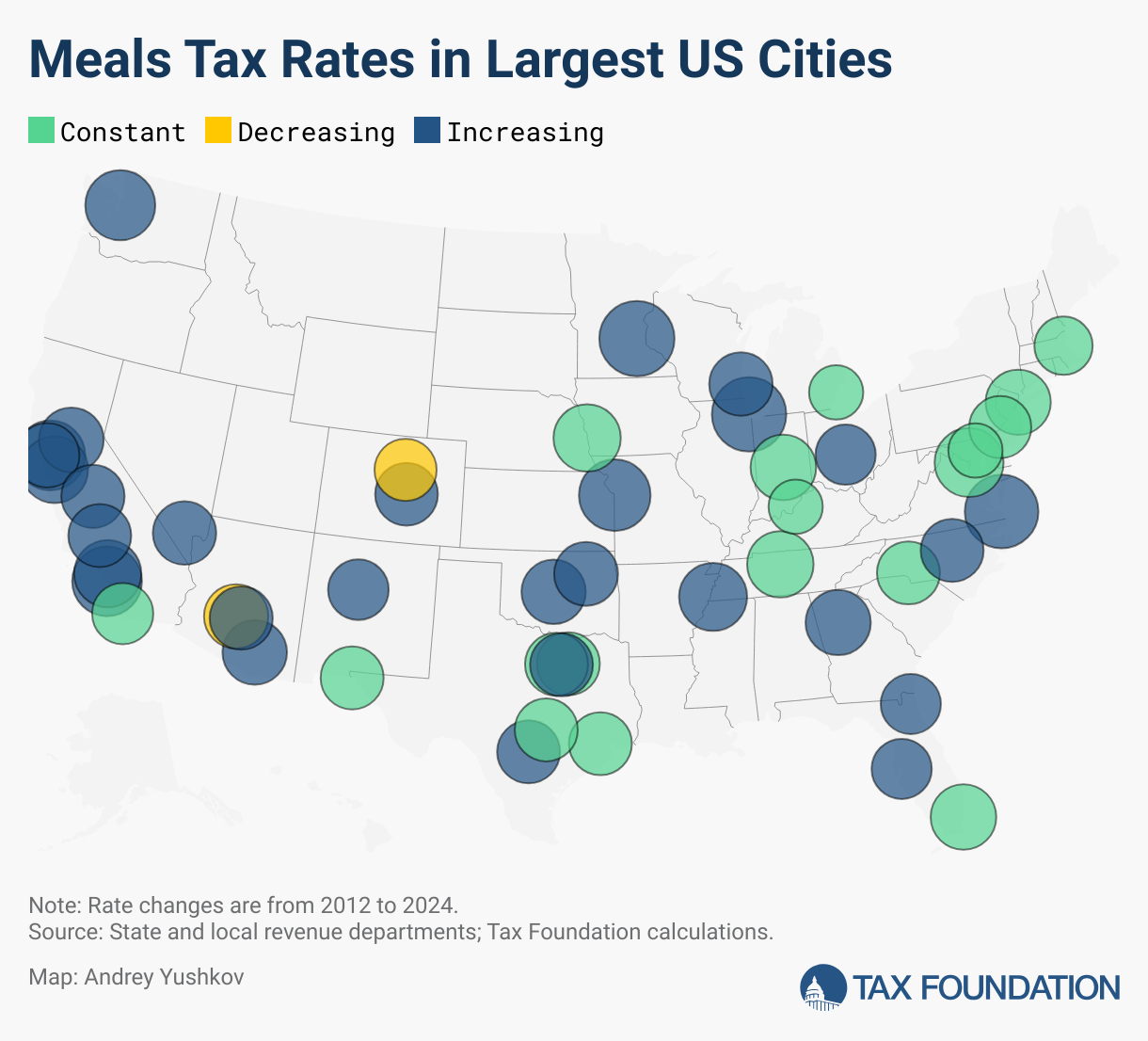

. Sales tax revenue increases automatically when you spend more on restaurant meals. It is attractive to have a consistent growth in the sales tax base, as most states’ bases are eroding. This is particularly true because it helps to cover gaps in other areas such as consumer digital goods and service that are not taxed yet in many states. The largest US cities have higher sales taxes than their smaller counterparts who live in states that allow local sales taxes. 13 of the 50 biggest cities also impose special meals taxes, which are taxes on purchases of ready-to-eat foods. 37 of these cities do not charge extra taxes on meals. The map and table below shows the rates that are applied to restaurant meals and prepared food in the 50 largest US Cities, as well as the changes in these rates from 2012 to 2020. Minneapolis, MN (12.03%), Chicago, IL (11.5%), Virginia Beach, VA (11.5%), Kansas City, MO (10.85%), and Seattle, WA (10.35%) have the highest combined tax rates for meals (including sales taxes and any additional meals taxes that may be applicable). Long Beach, Oakland, CA, as well as Washington, DC, have rates that are equal to or higher than 10 percent. Portland, OR is the only major city that does not impose a tax on restaurant meals. Oregon has opted out of a state sales tax and a city meal tax. In the largest cities with sales taxes, the lowest rates were found in Baltimore, MD, Detroit, MI, and Louisville, KY. Each of these cities had a 6 percent rate. All large cities in the West Coast except San Diego, CA saw an increase in meals taxes. The largest increases were in Milwaukee, WI (+2.3%), Kansas City, MO (+1.77%), Long Beach and Oakland (CA) (+1.5%), Minneapolis, MN (+1.15%%), and Tulsa (OK (+1.02%%). Some states, such as Massachusetts, Rhode Island and South Carolina, allow all counties or localities to impose a meals tax. Some states only allow certain localities, such as cities, counties or resort areas (such as Maryland), to impose meals taxes. New Hampshire and Vermont both have a statewide meal tax. State meals tax regimes, unlike those in the biggest cities, are relatively stable. They do not change frequently. A good practice from the perspective of transparency and neutrality–which is not followed by many states–is to limit any authorization for meals taxes to rates within a relatively narrow range and to avoid selective tax policies that apply only to specific cities or counties.Meals taxes are a meaningful source of (mostly) local consumption taxes in the US. As people dine at restaurants and similar establishments, or perhaps rely on prepared foods more at the grocery store, prepared food occupies an increasing share of personal consumption expenses and, therefore, a greater portion of sales. A narrow tax base can be inefficient and non-neutral. A broad tax base allows for lower tax rates and reduced administration costs.

. Since meals taxes are generally difficult to evade and avoid (data from the Bureau of Economic Analysis indicate that dining out does not decrease in places with relatively high meals taxes), they are an attractive revenue-generating tool for state and local policymakers.This does not, however, make them good policy. Higher taxes may not seem to affect dining out, but they still hurt people’s pockets. Policymakers should ask themselves why they are imposing this second tax. While the general sales tax is designed to fall on a broad range of consumption, special excise taxes are typically justified as ways to disincentivize behavior, internalize some negative externalityAn externality, in economics terms, is a side effect or consequence of an activity that is not reflected in the cost of that activity, and not primarily borne by those directly involved in said activity. Externalities can result from either the production or consumption of goods or services and can be positive.

None of this appears to apply to meal taxes. Local governments don’t try to make people eat out less. Eating prepared food does not have significant social costs for the government to cover. There are no additional governmental costs for people to dine out. The chief justification for a unique tax on meals would appear to be that dining is relatively inelastic and the tax is partly exported: people will dine out with or without the tax, and some decent share of the tax will be borne by nonresidents.

These considerations are not irrelevant, of course. Economists prefer taxes that don’t distort economic decisions. But special taxes on particular consumer choices should have some further justification as well, which is often lacking with meals taxes.

Furthermore, while special meals taxes generally meet the principle of revenue adequacy, policymakers should consider issues related to stability (as dining out often declines during times of crisis), transparency, and neutrality (since neighboring states and localities may have significantly different tax rates that are difficult to anticipate). States would be better off expanding the sales tax base so that it includes currently exempt categories of final consumption rather than imposing disproportionate taxes on prepared food. Until that happens, consumers should also be aware of high and rising meals tax rates in certain areas and plan their dining budgets accordingly.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe to our Newsletter

Share

TwitterLinkedInFacebook