The Activism Vulnerability Report | Q2 2022

With Labor Day marking the unofficial end of summer, FTI Consulting’s Activism and M&A Solutions team welcomes readers to our eleventh edition of the quarterly Activism Vulnerability Report, which reports the results of our Activism Vulnerability Screener following 2Q22, plus other notable trends and themes in the world of shareholder activism.

During 2Q22, the U.S. stock markets experienced considerable volatility as inflation remained a concern for investors. In July 2022, the U.S. Federal Reserve enacted its second consecutive 75 basis point interest rate increase, following a similar increase in the previous month. These factors, when combined with an inverted yield curve, early signs of a softening labor market and a second consecutive quarterly decline in GDP, have exacerbated investors’ concerns of a looming recession.

While the market has gained some ground from the lows of summer, as of September 1, 2022, the Dow Jones Industrial Average (“DJIA”) was down 12.9% year-to-date for 2022, the S&P 500 was lower by 16.8% and the Nasdaq Composite fell by 24.7%. Over the same period, the CBOE Volatility Index (“VIX”) was up over 30.2%.

While viewing the IPO and SPAC markets as proxies of market health and the appetite for large, risky investments, a dramatic trend unfolded in 1H22. Following 2021’s record-setting pace of IPOs on U.S. exchanges, IPO activity dropped precipitously in 2Q22, down to just 35 new listings as compared to approximately 200 in the same period last year. Last quarter was the weakest single quarter of IPO activity since 2017. Last year’s SPAC activity, which was partly sponsored by activist investors, also dried up, with many SPACs unable to complete the required acquisitions of operating businesses within the 24-month window. This rapid decline is a direct result of waning investor exuberance for high growth, marginal EBITDA companies amid unfavorable market conditions; at the same time, the SEC is proposing enhanced regulation on SPACs. Further illustrating this weakness, the gross proceeds from IPOs during the quarter were only $3.0 billion, the smallest quarterly total since 2016. This negative capital formation trend could continue as multiples of high-growth companies remain challenged.

Excluding SPACs, companies that went public in the United States in 2021 have seen their market caps drop by 44% on a weighted average basis from their listing prices, significantly more than the broader market. We expect that investors, including activists, have been and will continue to look for opportunities. During this price discovery process, we would not be surprised if activists uncovered opportunities that might not have been as apparent before the correction, and for those companies that activists have been eyeing, potentially lower valuations may have created more attractive risk/reward scenarios.

A total of 321 campaigns involving U.S.-based companies were launched in 1H22, with 164 in 1Q22 and 157 in 2Q22. The number of campaigns in 1H22 was up 23% compared to 1H21, and 2Q22 campaigns increased 45% from 2Q21, when there were 108 campaigns initiated. Activists managed to gain 31 of the 71 (44%) board seats sought in 2Q22, compared to 14 of 43 (33%) in 2Q21. In 2Q22, seven activist campaigns reached the final vote stage of their proxy contests, compared to 10 proxy contests reaching a final vote in the same period last year.

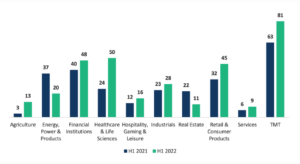

Technology, Media and Telecom (“TMT”) was the most targeted sector (of 10 total sectors) for shareholder activists in 1H22, representing 25% of all U.S. campaigns in the first half of the year, followed by Healthcare & Life Sciences (16%). The increase in activist campaigns against the Healthcare & Life Sciences industry may be, at least partially, driven by fluctuations in Biotechnology valuations. When compared to 1H21, Real Estate experienced the most notable decrease in activist attention, while the Agriculture sector saw the largest uptick, as determined by the percentage change in campaigns initiated.

Shareholder activists have continued to target large-cap companies (>$10 billion market-cap) at an increasing rate. In 1H22, large-cap companies represented 55% of all new U.S. activist campaigns, up from 50% of all campaigns in 1H21. Though high-profile activist funds remained active in 1H22, with firms like D.E. Shaw and Elliott Management launching notable campaigns at FedEx and Western Digital, respectively, a new trend has emerged that may transform the activism landscape.

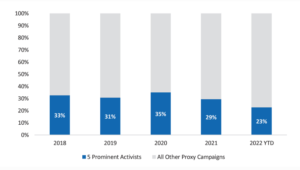

First-time activists accounted for a notable level (37%) of all campaigns initiated in 1H22, while some of the most familiar activist names (Elliott Management, Icahn Associates, Pershing Square Capital Management, Starboard Value and Third Point) accounted for only 23% of campaigns initiated during the six-month period, below concentration levels observed over the past five years. At their peak in 2012, the five funds noted above were particularly prominent in the world of shareholder activism and represented 39% of all proxy campaigns initiated. This may portend that activism is entering a new stage, evolving from the campaigns of the 2010s that often focused on cutting costs and returning cash to shareholders. This new stage is characterized by operational and strategic activism becoming fused with corporate governance and ESG. The current activism environment might be favorably positioned for first-time activists to be a driving force in shareholder activism and initiate more campaigns in the future. Despite prominent activists continuing to initiate larger-scale campaigns than their “first-timer” counterparts, we expect it will be more difficult for companies to predict activist playbooks and strategies in the future with so many new entrants in the field.

Activists Themselves are Not Immune to Activism

Over the last few decades, shareholder activists have invested in underperforming companies and agitated for changes designed to maximize shareholder value. Along the way, prominent activists have started insurance companies and closed-end funds, which gather additional capital for the activist and allow retail investors to benefit from the activist’s investment acumen. Recently, several London-listed, closed-end funds associated with activist firms have been subject to activist campaigns themselves. This ironic twist shows that shareholder activism plays no favorites and does not exempt any company, or fund, merely by virtue of who leads it.

The most recent example occurred at Trian Fund Management’s (“TFM”) UK-listed investment vehicle, Trian Investors 1 (“Trian 1”). TFM has over $7 billion in assets under management and has recently initiated a successful campaign against Unilever, as well as asset managers Janus Henderson and Invesco. Two of the fund’s founders currently serve on the Board of Janus Henderson. In June 2022, a group of shareholders at Trian 1 called for a special meeting to replace a majority of the fund’s Board, arguing that it was “the subject of board capture” and had “lost its independence” by serving the interest of outside parties. The group was led by Australian investment firm Global Value Fund, and rather ironically, included Invesco and Janus Henderson. At the special meeting in August 2022, shareholders managed to oust Trian 1’s Chairman, Chris Sherwell, in a tight ballot. Dissident nominee Robert Legget also was elected to the Board, while the other proposals by the investor group failed in a similarly tight ballot. Less than a month later, on September 2, Trian 1 management announced that it would wind down the fund by June 30, 2023. Investors will receive either the shares owned by the fund or cash.

In February 2022, activists achieved partial success against Third Point Investors Limited (“TPIL”), managed by Third Point. Third Point has run high-profile campaigns against Campbell Soup and Sotheby’s. In May 2021, British fund Asset Value Investors Limited (“AVI”) began a campaign against TPIL. Its suggestions included allowing shareholders to redeem some of their holdings at net asset value and replacing a director. Nine months later, TPIL settled with AVI and other shareholders who had joined its campaign, agreeing to add two new independent directors.

The fact that funds led, or managed, by activists can be subject to activist campaigns themselves is an interesting phenomenon. These campaigns have allowed activists to better understand the experience through a target’s eyes, which could change the approach by the activist in future campaigns. As the old saying goes, “It’s not personal. It’s strictly business.”

Continuing the trend from the end of 2021, and tracking with market volatility, many industries saw substantial changes in their vulnerability ranking in 2Q22 as six industries moved 10 or more spots. The Aviation & Airlines industry jumped 13 spots to the top of the list as the most vulnerable industry to activism, claiming the spot from the Biotechnology industry, which held the position for two consecutive quarters. Though the demand for air travel has returned as serious worries about the pandemic are subsiding, airlines have not been able to scale up operations accordingly. As a result, network fluidity has struggled and per unit costs remain elevated relative to airlines’ previous guidance, making the Aviation & Airlines industry more vulnerable this quarter.

Low-cost carrier Spirit Airlines was the subject of a successful hostile takeover bid earlier this year, which our team views as a form of corporate activism. Frontier Group and JetBlue Airways engaged in a four-month bidding war, with proxy advisors changing their recommendations based on the most recent bids. Spirit adjourned its shareholder meeting three times in an attempt to persuade shareholders to approve its proposed merger with Frontier. However, shareholders rejected that merger, resulting in Spirit finally agreeing to accept JetBlue’s unsolicited offer.

The airline industry is heavily regulated, which will make getting approval from the DOJ for JetBlue’s hostile takeover more difficult but still feasible. The Savings Banks and Insurance industries are also highly regulated. Both of those became significantly more vulnerable in the most recent quarter and both rank among our 10 most vulnerable industries. Savings Banks is now the second-most susceptible industry. In future quarters, banks may benefit from higher short-term interest rates, but also may be hindered by slower loan growth and increased loan delinquencies.

One notable campaign within the Savings Banks industry has been Driver Management’s attempt to add a new director at Philadelphia-based Republic First Bancorp. There has not yet been a vote on Driver Management’s nominee, but the company has replaced two directors, one of whom was its Chairman and CEO.

The Insurance industry also reversed course, jumping 13 spots and moving into the top 10 after trending down the list for the two previous quarters. While share price performance has been solid over the past year, insurers have noted multiple pain points stemming from inflationary pressure, such as increased costs related to claims and wage inflation required to retain and recruit talent.

Genworth Financial (“Genworth”), whose main business is life insurance, was the subject of a short-lived shareholder activism campaign earlier this year. Seven Corners Capital Management notified the company of its plan to nominate directors to Genworth’s Board, but later withdrew those nominations, instead urging shareholders to oppose four directors’ re-election and the company’s Say-on-Pay resolution. Shareholders approved all of Genworth’s nominees and resolutions at Genworth’s annual meeting.

Observations and Insights

“Activist funds have at least $200 billion of dedicated capital at their disposal, and they have started to deploy it aggressively. Based on Bloomberg, activist campaigns against U.S. targets were up by 10% during the first half 2022, and campaigns on companies with a market capitalization of $1 billion or more increased by 36% compared to last year. The recent market volatility, even a potential recession, is unlikely to deter activists. Activists are typically able to capitalize on market disruptions by initiating positions at lower prices, particularly those industries that have been most impacted, providing more upside than downside potential.

Unfortunately, the SEC added more fuel to the activism fire when it adopted the so-called ‘universal proxy’ rules, which have gone into effect on September 1, 2022. Under the previous rules, a company and an activist had separate proxy cards; shareholders could not easily ‘mix and match’ nominees across both slates. The new universal proxy rules changed this; both sides’ candidates will be on the proxy card. This seemingly innocuous change will have a dramatic impact on the U.S. activism landscape. While we had previously ‘slate contests’ where investors had a binary choice whether to support the company or the dissident, the new rules set up a ‘candidate contest’ where shareholders can choose preferred individual nominees. For one, this will make proxy contests more personal. The other practical effect is that there is a higher chance that the highly influential proxy advisory firms, ISS and Glass Lewis, will recommend for at least one dissident nominee. Similarly, vote-splitting by institutional investors will become more common. Sensing more leverage, activists are expected to demand more board seats in negotiations, making limited settlements with activists harder to achieve.

Companies ought to prepare by, among other things, (1) refreshing their boards to retire at-risk directors proactively, (2) preparing ‘break the glass’ communication plans in the event an activist attacks and (3) amending the bylaws to address some of the loopholes of the new universal proxy rules.”

— Kai Haakon E. Liekefett – Co-Chair of the Shareholder Activism & Corporate Defense Practice, Sidley Austin LLP

Although market volatility, as measured by the VIX, has steadily declined since June 2022, much uncertainty remains within the market as participants attempt to decipher rapidly evolving economic data to forecast the trajectory of our economy. Such uncertainty undoubtedly generated a great deal of investment hesitation in the second quarter, but newly depressed valuations may be too good to pass up, opening the door to a surge in campaigns through the end of the year. Further, as the Federal Reserve continues its work in hopes of curtailing inflation, investors may begin to see some light breaking through the clouds, giving them the confidence to deploy some of the dry powder that has been on the sidelines for the first half of 2022.

Endnotes

1Jonnelle Marte and Catarina Saraiva, Fed Hikes 75 Basis Points Second Time, Signals Third Is Possible, Bloomberg, (July 27, 2022), https://www.bloomberg.com/news/articles/2022-07-27/fed-raises-rates-by-75-basis-points-to-double-down-on-inflation.(go back)

2United States Rates & Bonds, Bloomberg (accessed on Aug. 23, 2022), https://www.bloomberg.com/markets/rates-bonds/government-bonds/us.(go back)

3Chelsea Bruce-Lockhart, Emma Lewis, and Tommy Stubbington, An inverted yield curve: why investors are watching closely, Financial Times, (April 6, 2022), https://ig.ft.com/the-yield-curve-explained/#:~:text=The%20gap%20between%20long%2Dterm,the%20harbinger%20of%20economic%20downturns.(go back)

4FTI Consulting analysis of market performance. Data provided by FactSet.(go back)

5Ibid.(go back)

6Sara B. Potter, U.S. IPO Activity Drops Dramatically in the First Half of 2022, FactSet, (July 14, 2022), https://insight.factset.com/u.s.-ipo-activity-drops-dramatically-in-the-first-half-of-2022#:~:text=According%20to%20FactSet%20data%2C%201073,raising%20just%20under%20%249%20billion.(go back)

7Ibid.(go back)

8Matthew Goldstein, SPACs Were All the Rage. Now, Not So Much., New York Times, (June 2, 2022), https://www.nytimes.com/2022/06/02/business/spacs-inflation-regulation.html.(go back)

9Sara B. Potter, U.S. IPO Activity Drops Dramatically in the First Half of 2022, FactSet, (July 14, 2022), https://insight.factset.com/u.s.-ipo-activity-drops-dramatically-in-the-first-half-of-2022#:~:text=According%20to%20FactSet%20data%2C%201073,raising%20just%20under%20%249%20billion.(go back)

10Crystal Tse and Katie Roof, US IPOs Can’t Shake 2022 Slump After Thriving Through Pandemic, Bloomberg, (June 28, 2022), https://www.bloomberg.com/news/articles/2022-06-28/us-ipos-can-t-shake-2022-slump-after-thriving-through-pandemic.(go back)

11FTI Consulting analysis of activist campaigns. Data provided by Insightia.(go back)

12Ibid.(go back)

13Ibid.(go back)

14Ibid.(go back)

15Ibid.(go back)

16Insightia – Shareholder Activism in H1 2022, Insightia, (July 2022), https://www.insightia.com/agh12022/.(go back)

17Lazard’s H1 2022 Review of Shareholder Activism, Lazard, (July 12, 2022), https://www.lazard.com/perspective/lazard-s-h1-2022-review-of-shareholder-activism/.(go back)

18Ibid.(go back)

19FTI Consulting analysis of activist campaigns. Data provided by Insightia.(go back)

20FTI Consulting analysis of activist campaigns. Data provided by FactSet.(go back)

21FTI Consulting analysis of activist campaigns. Data provided by Insightia.(go back)

22Greg Neer, How Closed-End Fund Activism Can Offer Value For Shareholders, RVP, (accessed August 23, 2022), https://rvpllc.com/how-closed-end-fund-activism-can-offer-value-for-shareholders/.(go back)

23FTI Consulting analysis of activist investors. Data provided by FactSet.(go back)

24Ad Hoc Committee (the “Committee”) of Independent Investors in T1H, Trian 1, (July 13, 2022), https://ti1independentinvestors.com/wp-content/uploads/2022/07/Ad-Hoc-Committee-Response-to-Trian-Investors-1-Limited-Circular-130722.pdf.(go back)

25Julie Steinberg, Shareholders Oust Chairman of Trian U.K. Fund, The Wall Street Journal, (August 8, 2022), https://www.wsj.com/livecoverage/stock-market-news-today-08-08-2022/card/shareholders-vote-to-oust-chairman-of-trian-u-k-fund-ZjHSVJKnPjQHUQwG34eN.(go back)

26Carolyn Cohn, Peltz’s Trian UK investment fund to close after campaign by activist investors, Reuters (September 2, 2022), https://www.reuters.com/business/finance/trian-uk-investment-fund-close-2022-09-02/.(go back)

27Ibid.(go back)

28FTI Consulting analysis of activist investors. Data provided by FactSet.(go back)

29AVI Public Letter to TPIL Shareholders, Asset Value Investors Limited (November 11, 2021), https://www.assetvalueinvestors.com/content/uploads/2021/11/AVI-Public-Letter-to-TPIL-Shareholders-11-NOV-2021_1.pdf.(go back)

30Third Point agrees truce with activist shareholders over UK fund, Financial Times, https://www.ft.com/content/3d773728-4d72-45ad-a042-0d2e3ef9d307.(go back)

31Megan Cerullo, Why are airlines canceling so many flights?, CBS News, (June 20, 2022), https://www.cbsnews.com/news/airlines-flights-canceled-delayed-cancellations/.(go back)

32Rajesh Kumar Singh and Abhijith Ganapavaram, JetBlue wins Spirit takeover battle with $3.8 billion deal, Reuters, (July 28, 2022), https://www.reuters.com/business/aerospace-defense/spirit-airlines-agrees-be-bought-by-jetblue-38-billion-deal-2022-07-28/.(go back)

33Elizabeth Dilts Marshall, Big U.S. banks see loan growth slowing as outlook for demand, economy darkens, Reuters, (July 18, 2022), https://www.reuters.com/business/finance/big-us-banks-see-loan-growth-slowing-outlook-demand-economy-darkens-2022-07-18/.(go back)

34Jeff Blumenthal, Activist investor nominates board candidate for Republic First Bancorp special election, Philadelphia Business Journals, (June 2, 2022), https://www.bizjournals.com/philadelphia/news/2022/06/02/activist-investor-nominates-board-candidate.html.(go back)

35David Mamane and Marlene Dailey, Insurance industry outlook: Summer 2022, RSM website, (June 6, 2022), https://rsmus.com/insights/industries/insurance/insurance-outlook.html.(go back)

36Proxy Statement of Seth Klarquist, United States Securities and Exchange Commission Schedule 14A, (April 7, 2022), https://www.sec.gov/Archives/edgar/data/0001276520/000176902222000031/gnwpreliminaryproxy472022.htm.(go back)

37United States Securities and Exchange Commission Form 8-K, (May 19, 2022), https://www.sec.gov/ix?doc=/Archives/edgar/data/0001276520/000119312522155127/d291171d8k.htm.(go back)

38FTI Consulting analysis of market performance. Data provided by FactSet.(go back)

39Ibid.(go back)