Placing Biden and Trump Tax Proposals in Historical Context

From President Biden calling the TaxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

Cuts and Jobs Act the “largest tax cut in American history,” to former President Trump claiming that Biden “wants to raise your taxes by four times,” the campaign rhetoric on taxes may be sparking some confusion.

To understand the magnitude of the candidates’ tax policies, we compare legislation enacted, tariffs imposed, and new campaign proposals from Biden and Trump to historical tax changes since 1940, averaging the annual revenue change of each law or proposal as a share of annual GDP over the years for which the data is available. (We rely on two data sources for the revenue effects of past tax bills: a US Treasury paper titled “Revenue Effects of Major Tax Bills,” and the Congressional Budget Office’s “Estimates of the Revenue Effects, in Billions of Dollars, of Legislation Enacted From 1981 to 2023 That Has a Significant Impact on Revenues.”)

Comparing Biden’s and Trump’s Tax Proposals

President Biden’s budget for FY 2025 proposes raising the corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.

rate from 21 percent to 28 percent, increasing the corporate alternative minimum tax from 15 percent to 21 percent, and increasing the top individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. imposes a progressive income tax where rates increase with income. The Federal Income Tax was established in 1913 with the ratification of the 16th Amendment. Though barely 100 years old, individual income taxes are the largest source of tax revenue in the U.S.

rate from 37 percent to 39.6 percent, among numerous other provisions.

On a gross basis, Biden would increase taxes by $4.4 trillion (an average of 1.19 percent of GDP per year) before reducing taxes by nearly $900 billion through expanded tax credits and preferences (an average of -0.25 percent of GDP per year). Together, the tax changes would increase average annual revenue by 0.94 percent of GDP, which would rank as the 9th largest tax increase since 1940 and the 2nd largest outside of wartime.

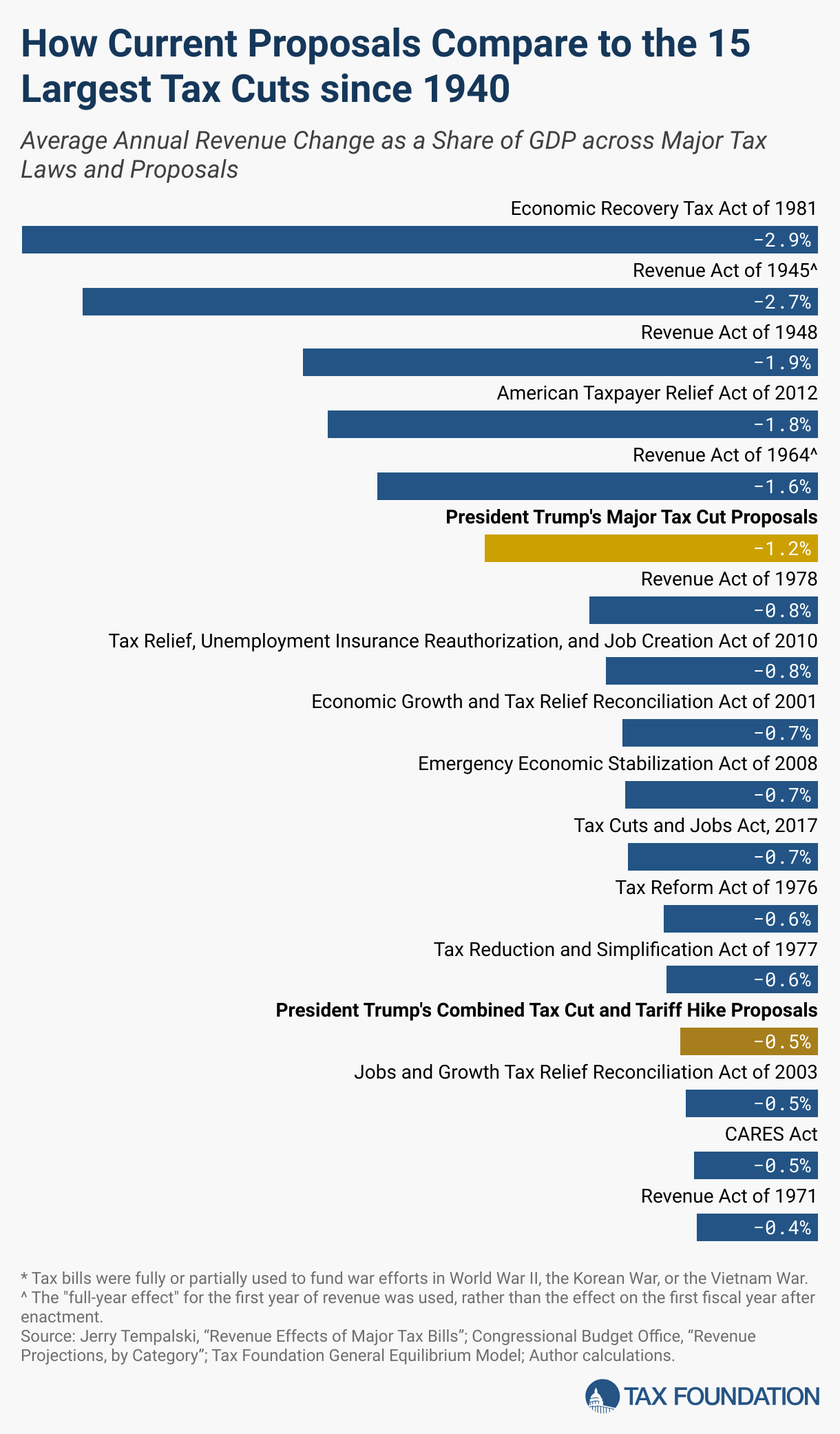

Although former President Trump has not released a formal tax plan for a potential second term, he has proposed several tax and tariff ideas, including new tariffTariffs are taxes imposed by one country on goods or services imported from another country. Tariffs are trade barriers that raise prices and reduce available quantities of goods and services for U.S. businesses and consumers.

hikes of 10 percent on all imports and 60 percent on Chinese goods, lowering the corporate income tax rate from 21 percent to 20 percent, and making the individual, estate, and business tax changes from the Tax Cuts and Jobs Act (TCJA) permanent.

In isolation, we estimate the proposed tariff hikes would increase average annual revenue by 0.71 percent of GDP, ranking as the 11th largest tax increase since 1940 and the 2nd largest outside of wartime.

Permanence for the TCJA would result in a gross tax cut of $7.4 trillion (reducing revenue by an average of -2.32 percent of GDP per year) before base broadeners of $3.2 trillion (increasing revenue by an average of 1.01 percent of GDP per year) bring the total 10-year cost down to $4.2 trillion. Combined with the lower corporate tax rate, Trump’s major tax proposals would reduce revenue by 1.21 percent of GDP on average, ranking as the 6th largest tax cut since 1940. Taken as a whole, Trump’s tax and tariff proposals would amount to a tax cut of 0.5 percent of GDP, ranking as the 13th largest tax cut enacted since 1940.

Where Do the Candidates Stand on Taxes?

Tax policy has become a significant focus of the US 2024 presidential election.

Compare 2024 Tax Plans

Largest Tax Increases since 1940

The five largest tax increases since 1940 all came during wartime from 1941 to 1951, raising revenue between 1.16 percent and 5.04 percent of GDP, on average. The Revenue Acts of 1941 and 1942 and the Current Tax Payment Act of 1943 helped finance defense spending during WWII, and the Revenue Acts of 1950 and 1951 helped fund the Korean War.

By comparison to the largest historical tax increases, the 2018-2019 tariffs imposed by President Trump on more than $380 billion of foreign products increased customs duties between 0.1 percent to 0.2 percent of GDP, ranking as the 21st largest tax hike since 1940. President Biden has continued the bulk of those tariffs and proposed further increases.

The Inflation Reduction Act (IRA) enacted under Biden ranks as the 23rd largest tax hike since 1940, increasing taxes by 0.1 percent of GDP in years with significant revenue effects (though the actual revenue effects of the IRA are highly uncertain given changing utilization and rules surrounding its energy tax credits).

Largest Tax Decreases since 1940

The five largest tax reductions since 1940 are the Revenue Acts of 1945, 1948, and 1964; the Economic Recovery Tax Act of 1981; and the American Taxpayer Relief Act of 2012. They reduced revenue by between 1.6 percent and 2.89 percent of GDP, on average.

The Revenue Acts of 1945 and 1948 were major postwar tax cuts to relieve Americans of heavy wartime tax burdens. The Revenue Act of 1964 was proposed by President Kennedy and signed into law by President Johnson to “reduce the drag on private purchasing power, profits, and employment,” significantly lowering both corporate and individual income taxes. The Economic Recovery Tax Act of 1981 was enacted under President Reagan, simplifying business taxation and significantly reducing individual income tax rates. The American Taxpayer Relief Act of 2012 extended many of the Bush-era tax cuts, among other tax changes.

By comparison to the largest historical tax cuts, the 2017 Tax Cuts and Jobs Act (TCJA) enacted under Trump ranks as the 10th largest tax cut since 1940, reducing tax revenues by an annual average of 0.69 percent of GDP, according to estimates from the Congressional Budget Office.

Pandemic-relief legislation also ranks relatively high, as policymakers under Trump and Biden relied on the tax code to distribute relief payments and support to individuals and businesses. Enacted under Trump, the CARES Act (-0.45 percent of GDP) ranks as the 14th largest tax cut since 1940, the Families First Coronavirus Response Act (-0.25 percent of GDP) as the 20th, and the Consolidated Appropriations Act of 2021 (- 0.15 percent of GDP) as the 26th. The American Rescue Plan Act (ARPA), enacted under Biden, would rank 20th based on its first two years of tax cuts (-0.25 percent of GDP), but incorporating the outyear effects, it falls to the 36th largest since 1940, at -0.08 percent of GDP overall.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

Share