Indiana Property Tax Reform Options

In Indiana, local taxes have been a major issue in this legislative session. The state’s

property taxes are primarily levied against immovable properties like land and buildings as well as tangible personal property which is movable like vehicles and equipment. Property taxes are the largest source of revenue for state and local governments in the U.S. They help fund schools, roads and police services, among other things.

The system has been nationally competitive for many years, but the dramatic increase in assessed values in recent years has created some discontent. Governor Mike Braun (R), proposed a reform to reduce the growth in property tax. A tax is a mandatory payment collected by local, State, and National governments from individuals and businesses to cover costs of general government goods, services, and activities.

bills. After several rounds of debate in the General Assembly both the Senate, and the House, introduced their own proposals for amending the structure of local tax in Indiana. While the debate continues, this blog post reviews the existing local tax system in Indiana, analyzes the major elements of each proposal, and discusses potential risks associated with replacing property taxes with local income taxes.The Existing Local Tax System in Indiana

Localities in Indiana have two primary sources of tax revenue: property taxes and local income taxes. Local income taxes are gaining in popularity, despite the fact that property taxes were traditionally the largest source of revenue. As of 2022, property taxes accounted for about 83 percent of local tax revenue, while local income taxes were at 12 percent.

Indiana’s property tax system ranks fifth best nationwide on our State Tax Competitiveness Index. The state sets property taxes as a percentage based on the assessed value of a property: 1 percent for residential property, 2 percent other residential property, 3 percent commercial property. Indiana offers generous homestead exclusions for owner-occupied dwellings. The state also imposes an annual levy cap (the maximum levy growth ratio, MLGQ) for all local governments. This limit is based on the growth in personal income over the past few years, as well as other socioeconomic factors. The MLGQ determines the maximum dollar amount each locality can collect in property taxes in a given year.

In recent years, median housing values, even adjusted for

inflationInflation is when the general price of goods and services increases across the economy, reducing the purchasing power of a currency and the value of certain assets. The same paycheck will cover less goods, bills, and services. It is sometimes called a “hidden” tax, as it makes taxpayers less wealthy due to increased costs and “bracket-creep”, while increasing government spending power.

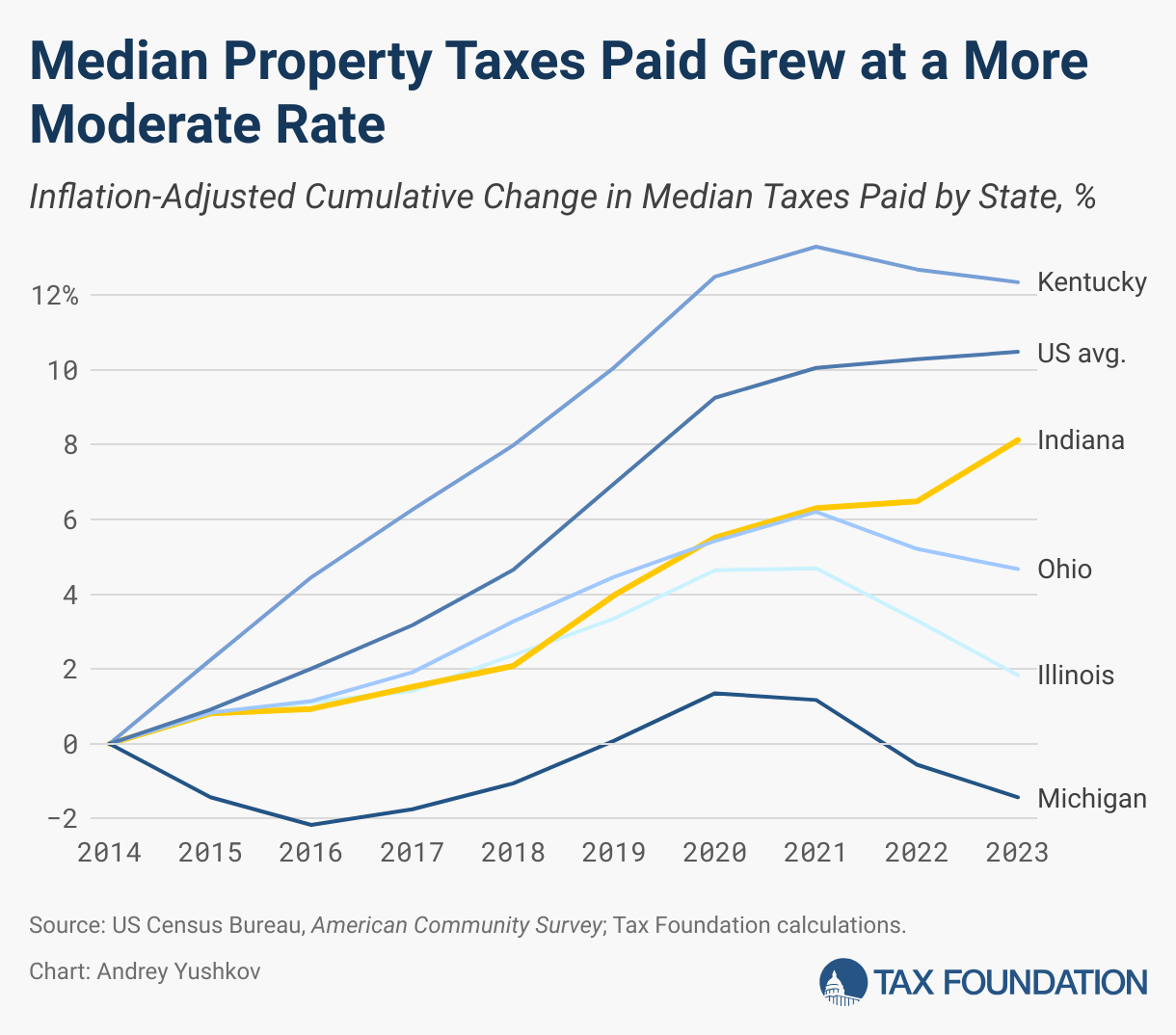

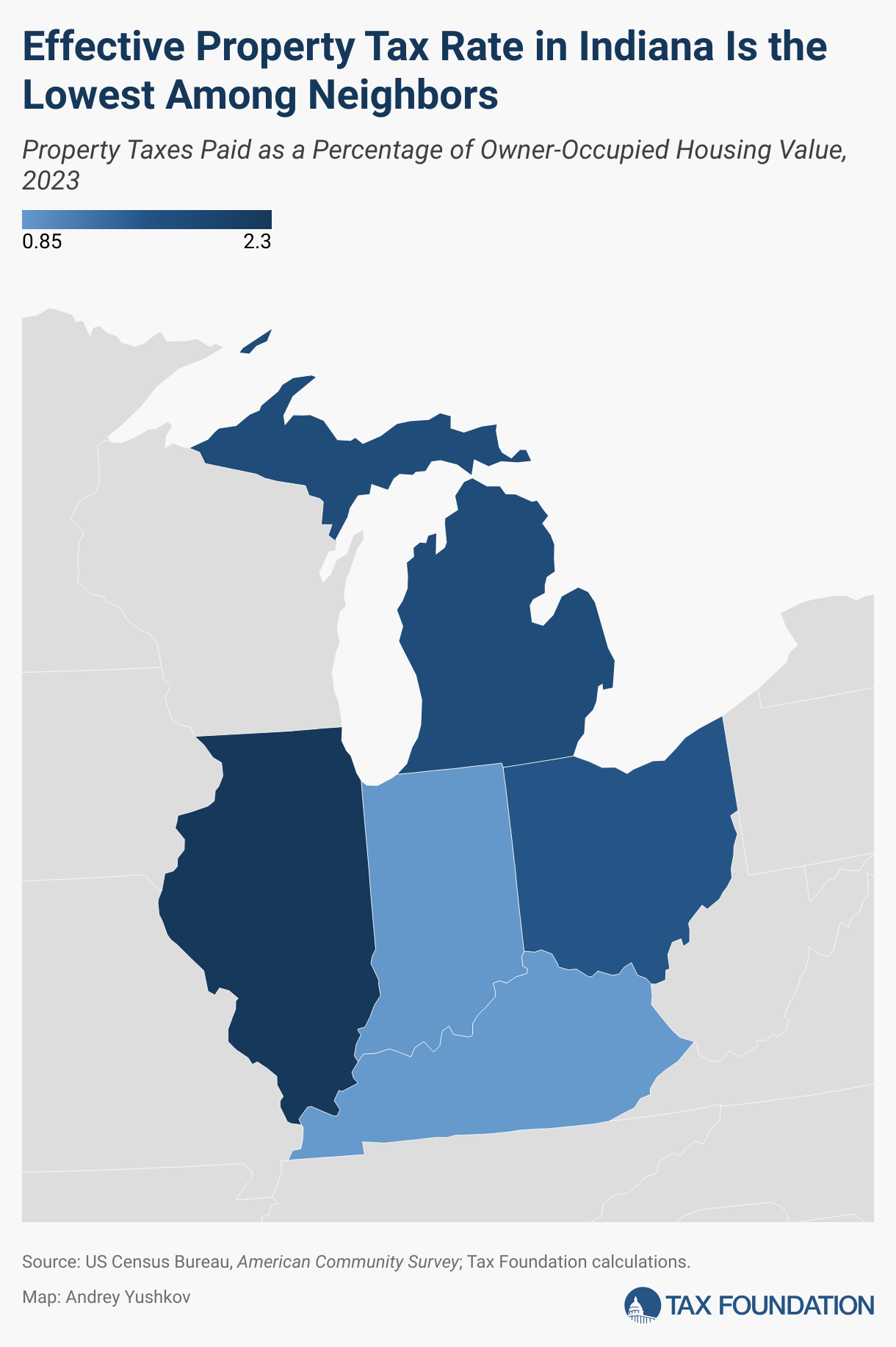

From 2014-2023, Indiana experienced a 27.6 percent appreciation of inflation-adjusted housing values. This was slightly lower than the national average (28.9 percent), but higher than all other neighboring states except Michigan. From 2014-2023, Indiana experienced a 27.6 percent appreciation of inflation-adjusted housing values, slightly lower than the nationwide average (28.9 percent) but higher than all other neighboring states except Michigan.At the same time, due to existing property tax limitations, inflation-adjusted median property taxes paid by homestead owners increased by 8.1 percent–lower than the nationwide average and Kentucky, but higher than in Ohio, Illinois, and Michigan.Overall, Indiana has had the lowest effective property tax burden among its neighbors since 2015. In 2023, Indiana homeowners paid an average of 0.74 percent of the value of an owner-occupied dwelling–lower than the nationwide average of 0.97 percent and the effective tax rates in Illinois (2.07 percent), Ohio (1.36 percent), Michigan (1.28 percent), and Kentucky (0.77 percent), indicating that the average cost of local services in Indiana is still relatively low compared to most other states.

However, local income tax rates have risen significantly since 2014, largely offsetting recent reductions in the state

individual income taxAn individual income tax (or personal income tax) is levied on the wages, salaries, investments, or other forms of income an individual or household earns. The U.S. has a progressive income taxes where rates increase as income increases. The Federal Income Tax was created in 1913, with the ratification 16th Amendment. Individual income taxes, which are only 100 years old but are the biggest source of tax revenue for the United States, have been around since 1913.

rate. The availability of the property-tax relief component in the combined local tax rate incentivizes counties to shift income from property taxes to income taxes. This leads to a greater variation in local tax rates throughout the state because of the lack of uniformity of local income policy. Greater reliance on local income taxes carries certain risks: it raises the overall income tax burden in the state, with limited state-level control over these increases; introduces a more volatile revenue source that tends to decline during economic downturns, especially compared to property taxes; and may negatively impact employment, particularly in the long run.Three ProposalsGov. Braun’s Original Proposal

While running for office, then-candidate Braun proposed significant changes to the existing property tax system, including increasing the homestead deduction and capping property tax bill increases. Under the plan, the modified homestead deduction would allow all homeowners with an assessed value over $125,000 to deduct 60 percent of the assessed value, with an even higher deduction for those with an assessed value below $125,000.

Currently, the owner of a home assessed at $400,000 can take a standard homestead deduction of $48,000 and a supplemental deduction of $132,000, totaling $180,000 or 45 percent of the assessed value. Under the proposed system they would be able deduct $240,000. The property tax bill increase would also be limited to 2 percent per annum for seniors, low income individuals, and families who have children under 18 and 3 percent for all other homeowners. As we have explained elsewhere, assessment limits are superficially appealing but ultimately result in wildly unequal tax burdens and make homeownership less affordable. As we have outlined elsewhere, assessment limits, while superficially appealing, ultimately yield wildly unequal tax burdens and make homeownership less affordable in the long run.

While the plan would provide relief to current homeowners (estimated to be around $1.3 billion in 2026, according to the fiscal note), it could create significant revenue shortfalls for local governments, particularly cities and school districts (they would lose $263 million and $536 million, respectively), limiting their ability to provide services or incentivizing them to seek alternative revenue sources.

Senate Amendments

The amended version of Senate Bill 1, introduced by Sen. Travis Holdman (R), presented a different vision for the local tax reform. Instead of increasing the homestead deduction and capping property tax bills, the revised bill included a more moderate set of proposals.

Specifically, the amended version implemented a significantly stricter levy limit, capping the MLGQ at 0-2 percent for 2026-2028 and modifying its formula thereafter. It also introduced a local property tax deferral, which allows qualified homeowners to defer property taxes up to $10,000 per year. The bill also established the

tax credits for first-time homebuyers. A tax credit is a provision which reduces a taxpayer’s final tax bill dollar-for-dollar. Tax credits are different from deductions and exclusions, which reduce the taxpayer’s final tax bill by dollar-for-dollar.

, enabling new homeowners to receive a credit of up to $2,500 for up to five consecutive years in which they have a property tax liability for their homestead.

Other provisions of the amended bill included higher targeted deductions and circuit breaker credits for certain retirees and disabled veterans, new rules for tax referenda and excess levy appeals, and various other minor adjustments.According to the fiscal note, the proposed relief for homestead owners would be considerably more limited in scope, ranging from $91 million in 2026 to $254 million in 2028. At the same time, cities and school districts would experience revenue losses of $50 million and $61 million in 2026, and $150 million and $183 million in 2028, respectively.House Amendments

House Bill 1402 represents a third approach. The bill would increase de minimis exemptions for tangible personal properties from $80,000 up to $200,000, and introduce a new full exemption for business personal property. These changes would continue providing tax relief and reducing compliance costs for small and medium-sized businesses.

Additionally, the bill outlines a gradual transition to a flat supplemental homestead exemption equal to two-thirds (67 percent) of the assessed value, accompanied by the phaseout of the standard homestead deduction. This proposal is in line with Gov. Braun’s plan is simplified further. The bill also introduced a deduction for all properties subject to the 2 percent credit for circuit breakers, which would gradually phase-in by 2031.

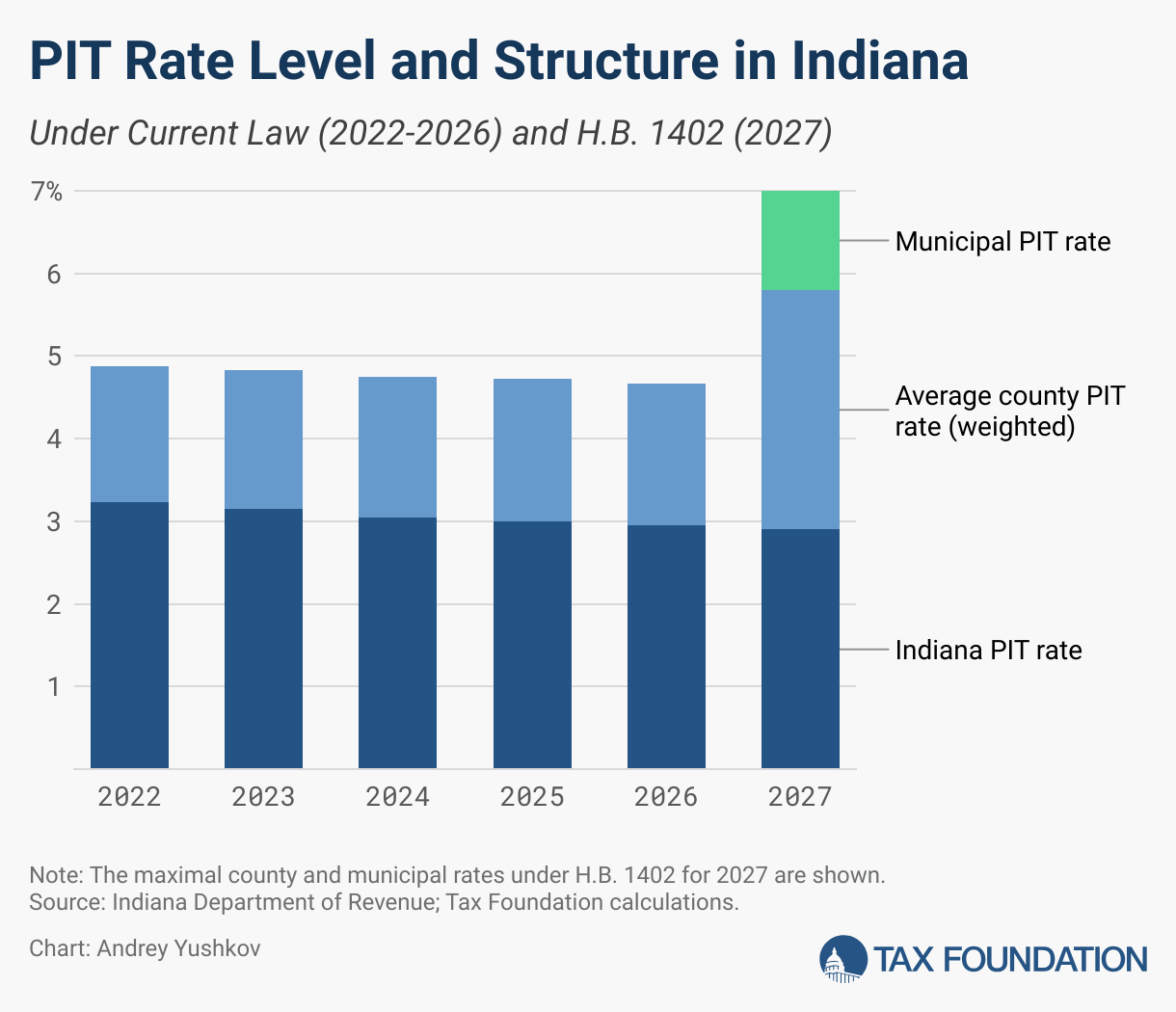

. However, the most problematic aspect of this bill is its radical restructuring of the local tax system. The proposal would set the maximum local income tax at 2.9 percent in counties and 1.2 per cent for cities and towns that have a population of 3,500 people or more. Currently, only counties can impose this tax. If this restructuring is combined along with property tax reductions that were part of an earlier proposal, counties and municipalities will have strong incentives for raising their local income taxes to the maximum level. The state’s income tax rate (now at 3%) has been steadily declining over the past few years. However, a significant increase in local income taxes could push the combined state and city income tax rate up to 7 percent in 2027 – assuming that all counties and cities adopt this maximum rate. This would be a much higher rate than the current combined tax of just under 5%. This could mean that the recent Indiana income tax reforms would be completely offset by a potential local tax shift. This would be higher than rates in Illinois, Michigan, or Kentucky, which are all neighbors. As of 2022, the average effective local income tax rate in Michigan and Kentucky was 0.18 percent, while Illinois did not have local income taxes. Levy limits can be a more neutral and efficient tool to keep property tax bills in check (and revenues), and the existing levy cap allows for further refinement. If policymakers believe this limit still allows for an inequitable distribution of the property tax burden across different property classes, they could modify it to ensure tighter control over levy growth from each class (e.g., property tax levies from each class should not exceed the greater of 5 percent or the MLGQ).

Finally, shifting property tax revenue to local income taxes is not a growth-oriented strategy. Income taxes can be more distorting than property taxes, and influence the decisions of both current and future Indiana residents. Individuals with a high income may consider moving to a state without income taxes, while any Indiana resident could decide to move to a county that has a lower income tax burden. To maintain its competitive tax system, the state should prioritize keeping local income tax rates relatively low and within a narrow range (currently, rates vary from 0.5 percent in Porter County to 3 percent in Randolph County). To maintain its competitive tax system, the state should prioritize keeping local income tax rates relatively low and within a narrow range (currently, rates vary from 0.5 percent in Porter County to 3 percent in Randolph County) instead of incentivizing counties and cities to significantly increase the income tax burden.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe to our Newsletter