Germany Trade Tax Rates | Tax Foundation

Businesses in Germany are taxed on their corporate income at an average rate close to 30 percent. However, their taxA tax is a mandatory payment or charge collected by local, state, and national governments from individuals or businesses to cover the costs of general government services, goods, and activities.

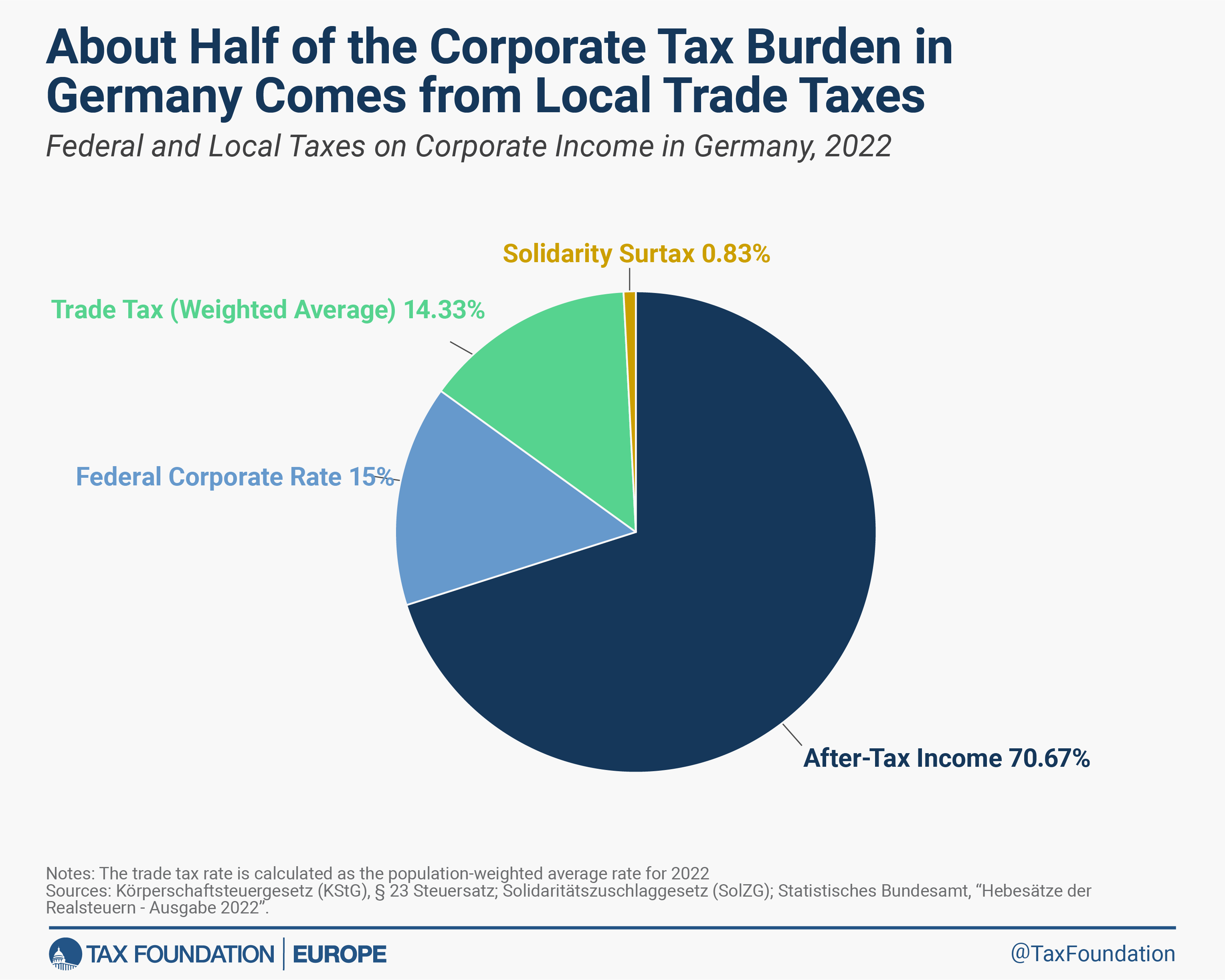

burden can vary substantially depending on their location, as only about half of it is levied at a uniform 15 percent corporate income taxA corporate income tax (CIT) is levied by federal and state governments on business profits. Many companies are not subject to the CIT because they are taxed as pass-through businesses, with income reportable under the individual income tax.

rate subject to a 5.5 percent solidarity surtaxA surtax is an additional tax levied on top of an already existing business or individual tax and can have a flat or progressive rate structure. Surtaxes are typically enacted to fund a specific program or initiative, whereas revenue from broader-based taxes, like the individual income tax, typically cover a multitude of programs and services.

. The remainder of the corporate rate depends on local trade taxes across the country’s 10,786 municipalities that can set their rates autonomously, subject to a minimum rate of 7 percent. This structure has important consequences for Germany’s attractiveness for business investment as well as local governments’ revenue stability.

Generally, local tax competition can be beneficial by allowing individuals and businesses to choose more attractive combinations of tax rates and publicly provided goods and services. The benefits of this sort of location competition increase along with local governments’ decision-making autonomy over the relevant location factors. In Germany, these may include the resources dedicated to local bureaucracy, permitting, and some infrastructure, while many other factors are either at the state or federal level. In federally organized countries like Germany, Spain, or Switzerland, tax competition can prevent national tax policy from becoming less attractive than if it were organized at a central government level.

In practice, local tax competition over trade tax rates is weakened by fiscal transfers between municipalities and local government commitment problems. Empirical research finds that local governments face substantial problems in making credible commitments to low trade tax rates. When firms make large, immobile investments relative to municipality size, municipalities respond by increasing their trade tax rate by up to 24 percent. This hinders business investment in immobile assets, such as power plants, as firms anticipate subsequent hikes in the tax rate.

Compared to property taxes or local governments’ assigned shares of local value-added tax (VAT) and personal income tax revenues, local trade taxes can be an unstable source of revenue, especially for small jurisdictions with local economic activity concentrated in a few businesses. In recent years, concerns over the revenue stability of smaller municipalities have motivated restrictions on net operating loss carrybacks. Businesses in Germany are currently only allowed to offset current losses from the past two years’ profits against the corporate tax, but not against the local trade tax. This restriction disproportionately deters investment in projects with highly variable profits and losses, such as start-ups and R&D-intensive businesses.

The simple average trade tax rate is 12.89 percent, ranging from the minimum rate of 7 percent levied in Langenwolschendorf’s (Thuringia) up to 22.75 percent in Inden (North-Rhine Westphalia). The population-weighted average rate is 14.33 percent, about 1.5 percentage points higher than the simple average, as larger municipalities tend to have higher trade tax rates.

The 10 largest German cities, Berlin (14.35 percent), Hamburg (16.4 percent), Munich (17.15 percent), Cologne (16.625 percent), Frankfurt am Main (16.1 percent), Stuttgart (14.7 percent), Duesseldorf (15.4 percent), Leipzig (16.1 percent), Dortmund (16.98 percent), and Essen (16.8 percent), all levy higher-than-average trade tax rates. Higher rates in those large cities may reflect the benefits of firms clustering together in close proximity that reduce their mobility and thus allow local authorities to levy relatively higher taxes on them. Yet, large German cities still compete over trade tax rates with both neighbouring suburban municipalities and other large cities.

Rates also differ across different states of Germany. The city-state governments of Bremen and Hamburg as well as local governments in North-Rhine Westphalia and Saarland tend to levy the highest rates while local governments in Bavaria and Brandenburg levy the lowest rates. Local governments can leverage lower trade tax rates—especially in comparison to jurisdictions with similar location factors—to attract business investment.

Stay informed on the tax policies impacting you.

Subscribe to get insights from our trusted experts delivered straight to your inbox.

Subscribe

Share